As the end of the financial year approaches, it is important that you take the time to focus on tax planning and tax issues that affect your clients before 30 June 2024 arrives. We have outlined some of the key tax considerations below:

Prepaid Expenses

Expenses are deductible when they are incurred. For an individual this is when the expenses are paid, therefore wherever possible pay for deductible expenses prior to 30 June. This includes insurance and interest on rental properties.

Income Protection Insurance

A deduction is available for the cost of insurance to cover loss of income if you paid for it in full before 30th June.

Income Protection Insurance

This is a great strategy for those with not many deductions.

The contribution caps are currently: ⦁ Concessional Contribution: $27,500 per annum. ⦁ Non-Concessional Contribution: $110,000 per annum. The ability for a member to contribute is dependent on their age and Total Superannuation Balance (TSB) at the previous 30 June. To make non-concessional contributions, a member’s Total Superannuation Balance must be less than $1,700,000 at the previous 30 June.

Eligibility for Super Co-Contribution

You will be eligible for the government super co-contribution (max. of $500 in 2022-23) if you meet the following eligibility criteria: ⦁ You made personal super contributions to your superannuation account during the financial year (max. $1,000). ⦁ Your total income is less than $58,445. ⦁ 10% comes from employment related activities or carrying on a business. ⦁ You were less than 71 years old at the end of the financial year.

Working From Home Deduction

If you are planning to claim working from home expenses in your 2023-2024 tax return, one of two methods is available to you. Either the Fixed Rate Method or the Actual Cost Method.

Fixed Rate Method

⦁ This is a fixed rate of 67 cents per hour worked from home. ⦁ You no longer need a dedicated home office. ⦁ The 67 cent rate per hour includes the claim for electricity and gas, phone and internet usage, computer consumables and stationery. ⦁ You can’t claim Internet or utilities with this method. ⦁ Allows you to separately claim amounts for expenses not covered by the revised fixed rate, such as the decline in value of depreciating assets and the cost to clean a dedicated home office. ⦁ You must keep a record of all hours worked from home during the financial year.

Actual Cost Method

⦁ This is the additional expenses you incur as a result of working from home at a certain percentage, not 100% of your bills

⦁ Additional running expenses may include

– Electricity or gas (energy expenses) for heating or cooling and lighting. – Home and mobile internet or data expenses. – Mobile and home phone expenses. – Stationery and office supplies. – The decline in value of depreciating assets you use for work. – For example, office furniture such as chairs and desks. – Equipment such as computers, laptops and software. – The repairs and maintenance to depreciating assets. – You must have records that show you incur these expenses.

Motor Vehicle

If you use your motor vehicle for work related purposes, the following two methods can be used to calculate your deduction: Cents per kilometre ⦁ 85 cents per km for each business kilometre for the 2024 financial year. ⦁ Claim to a maximum of 5,000 business kms. Logbook method ⦁ Based on the business use percentage as per the logbook records. ⦁ Odometer readings are required at the start and the end of the period. ⦁ Written evidence of expenses is required. Of late, the ATO has allocated their resources to audit investigations, particularly on substantiation records and logbooks. Ensure your logbook is up to date. There are many cost-effective electronic methods of recording odometer readings for logbook recording.

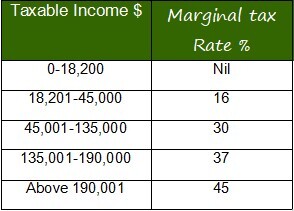

Personal Income Tax Rates

Please do not confuse, the tax cuts start on 01st July 2024

The 2024 marginal tax rates are shown below: ⦁ Taxable income up to $18,200: 0% Rate ⦁ Taxable income from $18,201 to $45,000: 19.0% Rate ⦁ Taxable income from $45,001 to $120,000: 32.5% Rate ⦁ Taxable income from $120,001 to $180,000: 37.0% Rate ⦁ Taxable income over $180,001: 45.0% Rate These rates do not include the Medicare Levy (currently at 2%).

HELP, SSL, ABSTUDY SSL, TSL and SFSS Repayment Threshold

HELP Changes

Indexation Formula Reform: ⦁ Indexation rate will be the lower of the Consumer Price Index (CPI) or Wage Price Index (WPI) ⦁ Applies to all HELP, VET Student Loans, Australian Apprenticeship Support Loans, and other student loan accounts existing on 1 June 2023. ⦁ Automatic Adjustments: The ATO will adjust outstanding HELP loan balances indexed on 1 June 2023 and 1 June 2024, applying any resulting credit to the individual’s HELP account. The repayment threshold for the 2023-24 financial year is $51,550 or above. Once an individual’s taxable income is above this threshold, a repayment of the debt is payable on the lodgement of the individual’s tax return.

Travel Expenses

A deduction can be claimed for the expenses incurred in travelling for work related business purposes. If you did not receive a travel allowance: ⦁ and travel is less than six nights in a row: – written evidence is required (such as receipts for meals, hotels, taxis, etc), but a travel diary is not required. ⦁ and travel more than six nights in a row: – written evidence is required (such as receipts for meals, hotels, taxis, etc), and a travel diary is required.

Medicare Levy – Low-Income Thresholds

You may know if your income is low, you may get Medicare for free.

The Medicare levy low-income threshold is $26,000 for individuals, $43,846 for families (with no children) and $41,089 for seniors and pensioners for the 2023-2024 income year.

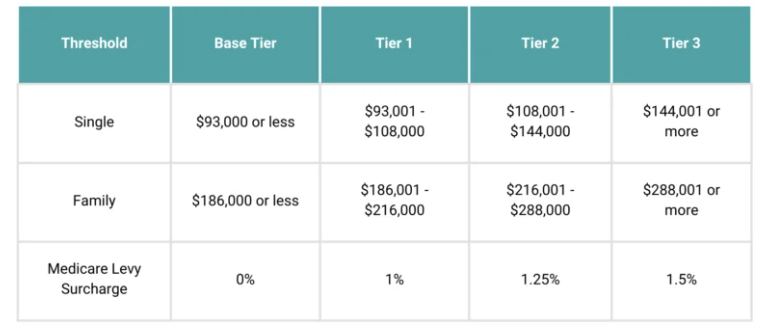

Private Health Insurance and Medicare Levy Surcharge

The rebate levels for 2023-2024:

The family income threshold has increased by $1,500 for each MLS dependent child after the first child.

Depreciation

If you purchase assets which will be used to generate income for several years (i.e. purchasing a new oven for a rental property), you can claim a decline in value (depreciation) each year. We would recommend using a business (such as ‘Depreciator’) to prepare a depreciation schedule for rental properties, on your behalf. This schedule can be used to: ⦁ Obtain a Quantity Surveyor’s report on any rental property Australia wide; or ⦁ Obtain a report listing depreciation entitlements for that property on a yearly basis. Therefore, if you have recently purchased a rental property, please contact us to discuss the preparation of a depreciation schedule.

Tax Cuts – Tax Rates from 01 July 2024

Substantiation

To claim your personal tax deductions, ensure you can substantiate your expenses: ⦁ Claims exceeding $300 must be supported by written evidence for the entire amount, not just the amount over $300. ⦁ The $300 limit does not include award transport payments or car, meal, or travel allowance expenses. ⦁ For expenses $10 or less, provided in total they do not exceed $200, a written note detailing the same information as on a receipt (in a diary for example) is sufficient where you cannot obtain a receipt.

More information

⦁ If you have any questions, feel free to get in touch with us on 03 9885 4554 or drop us an email.

“Liability is limited by a scheme approved under Professional Standards Legislation”